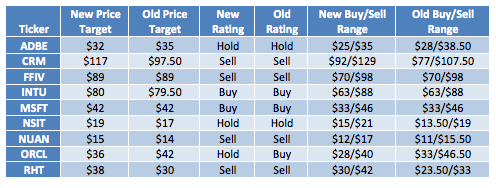

The chart below shows new ratings, price targets, and buy/sell ranges vs. old ones:

(click to enlarge)

Adobe:

Maintain at Hold, Decrease PT From $35 To $32

Adobe:

Maintain at Hold, Decrease PT From $35 To $32For Adobe, we maintain that the stock is pretty fair valued at its current place. We did, however, decrease our price target from our last update. The reason for our drop in price target was we saw a hit to equity value. That drop came from a decrease in cash holdings for the company, lowered expectations for the FY for the company in operating income, as well as an increase in expected changes in working capital that we had underestimated. The company's cash holdings dropped by over $100M quarter to quarter.

Additionally, we had predicted a fairly flat growth rate in working capital, but that has increased around $400M in the TTM. Finally, we slightly lowered our expectations for the company for the quarter. The company did recently announce that it will be doing a share repurchase program through the end of 2015 worth $2B that will positively influence shares outstanding, but we did not believe that outweighed some recent changes we saw.

Salesforce.com: Maintain At Sell, Increase PT from $97.50 to $117

The valuations on CRM continue to amaze us. Right now, the stock sits with a 75 future PE, which is really quite significant. While we do see a lot of future value in this company and very strong growth rate, the company is far exceeding any future growth rates. We believe our model is a best-case scenario model that sees CRM at around $1B in operating income in 2015, a very low discount rate due to its high growth model, and strong depreciation growth.

Even with these inputs, we do not seem to be able to justify a $150 price. The only way we can get to that price is if CRM could achieve around $1.5B in operating income by 2015. That growth model is extremely excessive and unreasonable. Therefore, while we understand the high-growth and strong brand name the company is building, we do not agree that the valuation is reasonable.

F5 Networks: Maintain At Sell, Increase PT from $89 to $108

F5 is very similar to CRM in that its a high-growth application software company in the cloud network with excessive valuations. FFIV is much more realistic with a 22+ forward PE ratio on our model. The issue we have with FFIV is that the company is once again probably pricing in a bit above expectations. We have given the company a model that prices in $750M in operating income by 2015, which is once again about a best-case scenario.

Additionally, we believe that the company suffers in our model from high capital expenditures. While we understand that capex is an investment in the future, we worry that the market does not seem to price in the current negative it has on equity value, which is part of the reason for its overpricing. We believe that the company is closer to valuation than CRM, but we still believe that upside is less than for other better value plays.

Intuit: Maintain at Buy, Increase PT From $79.50 to $80

Most everything remained the same at Intuit since our last update. We removed half dollar valuations, which is the reason for the minute price target increase. Recent results were in line with expectations and no major changes were made. We believe recent weakness has provided a nice entry point to a company with solid growth, good value, and a decent economic moat.

Microsoft: Maintain at Buy, Maintain PT at $42

The latest results were actually slightly under our expectations for the company, but they were fairly strong results. Our price target came out neutral following our latest update as cash and cash equivalents fell from previous levels, which did hurt equity value. At the same time, though, the drop in FCF did raise net debt slightly, which gave us a slightly lower WACC that made up for the shift lower in cash. These were slight changes that were not overly impactful to the overall outlook of the company.

We remain bullish on the company and believe that it is very undervalued at current levels. It is operating a 10.6 future PE ratio, which is well below industry averages with a strong brand name and decent economic moat especially in some sides of their business like Word. Further, the company is doing well in its server business, which is a strong growth market for the company that should continue to do well.

Insight Enterprises: Maintain at Hold, Increase PT from $17 to $19

We slightly increased our expectations for NSIT after its latest round of results outperformed our expectations. The company is a great value stock at current levels, but we do see some decent risk with the company. It has a lower growth model and barely any economic moat at all. We raised our price target for the company, though, due to its drop in WACC as beta on the stock was lowered, which gave it a lower discount rate. High-beta stocks are discounted at a higher rate due to more risk. Expectations are actually slightly under expectations, and until the company drops debt and shows more growth, we see it as pretty fair valued.

Nuance Communications: Maintain at Sell, Increase PT from $14 to $15

Despite the company's slight outperformance in its recent earnings, we still are not sold as to the Nuance stock. First off, the stock has a 154 PE ratio, and we do not believe that even if the company's future PE is much lower that the company has not baked in a lot of future earnings. It has. The company has a lot of excitement over its unique software, which we understand, but the company's growth is strong, but not overly aggressive.

We upped our PT as shares outstanding dropped, cash was up, and the company slightly outpaced our expectations. At the same time, we still have a fairly aggressive model in place that sees about 100% growth in operating income through 2015. We believe that at this time the stock has priced in a lot of future growth, and upside is limited.

Oracle: Downgrade from Buy to Hold, Decrease PT from $42 to $36

The recent earnings of Oracle were fairly in line with our expectations, but we dropped our price target as the tax rate increased and expectations were lowered slightly. The tax rate jumped from 29% to now 33%, and that jump does weaken equity value rather considerably. The company, additionally, slightly underperformed our expectations for them for their latest quarter, and we reduced our expectations moving forward. Right now, we do believe it has a lot of value with a growing cloud software division, but it has not done as well as we had expected with it.

Redhat: Maintain at Sell, Increase PT from $30 to $38

The valuations on Redhat are out of control right now. The company is sitting at a 42 future PE, and the stock has just gone way too far, way too fast. The company benefited a lot from its latest quarterly results, which were slightly above expectations. Yet, the latest results continue to over-exagerate the company's recent success.

We raised our price target as the company increased cash and was lowered to a smaller discount rate due to more cash holdings. At the same time, we have an aggressive model in place for RHT with 90% growth in operating income in the next five years. Right now, the company is vastly overvalued, and its a good time to Sell if you hold.

No comments:

Post a Comment