Global Macro Notes: Falling Bonds, Rising Transports, Vulnerable Aussie

Overbought conditions can be resolved in one of two ways: Either through

price or through time.

The major U.S. indices appear to be resolving through time, grinding sideways rather than correcting lower. The potential for a fear-induced sell-off catalyst remains high, but bulls are gaining traction.

(click to enlarge)

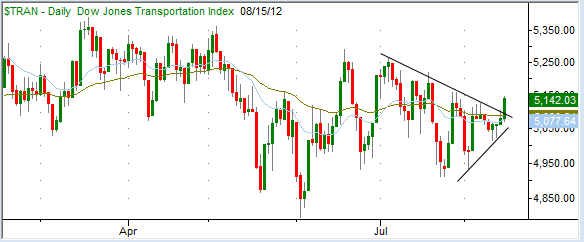

The Dow Transports were previously non-committal, a fly in the ointment of the bull case for the major U.S. indices. On Wednesday the Trannies resolved bullish.

(click to enlarge)

In further bullish confirmation, long bonds are accelerating to the downside, suggesting a rotation out of safe havens and into risk assets.

What is some possible reasoning for this?

In addition to the central bank "wrapper" - bad news gets stimulus, good news means equities still king in a zero-interest world - general perception may be sinking in that Europe has stabilized. This could be a completely wrong perception, but absence of a fear-mongering macro catalyst (at least in the short run) lends a strong argument to equities.

Conditions remain hostile with macro risk elevated and the VIX at low extremes. The counter to this is that the VIX can stay low for extended periods of time, as equities grind higher in the absence of fear catalysts.

Notable piece from WSJ on reaching for yield down under. In-flows into Australian bonds have kept the currency strong.This phenomenon is interesting for multiple reasons:

(click to enlarge)

The source of AUDUSD strength explained. This presents a clearer picture of why the Aussie dollar short-term bottomed on July 1, 2012. Incoming capital flows buoyed the currency.

Dangerous assumptions re, China revealed. Those "reaching for yield" via Australian debt are implicitly assuming China's hard landing will not destabilize Australia's heavily natural-resource-leveraged economy (with housing bubble to go with). This could prove an exceptionally bad assumption.

Potential double negative for AUDUSD moving forward. If the global slowdown grows more serious, strongly impacting base metals prices - as others have noted, copper looks very vulnerable - then assumptions of China avoiding a hard landing could be proven false, severe decline in base metals prices could follow, and the double down Aussie carry trade could unwind in severe fashion.

On the other hand, if the "risk on" rally in Western assets appears sustainable, AUDUSD could decline anyway as foreign capital withdraws from Australian debt holdings and returns to local opportunities.

In this low conviction macro environment, we still very much like the big-picture drivers for short AUDUSD.

How crappy has forex been as a return generator these past few years? Epically crappy:

More Bullish Setups

Part of our process involves scanning hundreds of charts (typically 400+), both mechanically and visually, on a daily basis. The feedback of this scan gives additional flavor as to the character and positioning of the market.

We are starting to see more bullish setups pop up now, and more winning stocks separate themselves from losing stocks. The picture is consistent with bulls gaining traction as overbought conditions resolve through time rather than price.

Notable technical developments:

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

The major U.S. indices appear to be resolving through time, grinding sideways rather than correcting lower. The potential for a fear-induced sell-off catalyst remains high, but bulls are gaining traction.

(click to enlarge)

The Dow Transports were previously non-committal, a fly in the ointment of the bull case for the major U.S. indices. On Wednesday the Trannies resolved bullish.

(click to enlarge)

In further bullish confirmation, long bonds are accelerating to the downside, suggesting a rotation out of safe havens and into risk assets.

What is some possible reasoning for this?

In addition to the central bank "wrapper" - bad news gets stimulus, good news means equities still king in a zero-interest world - general perception may be sinking in that Europe has stabilized. This could be a completely wrong perception, but absence of a fear-mongering macro catalyst (at least in the short run) lends a strong argument to equities.

Conditions remain hostile with macro risk elevated and the VIX at low extremes. The counter to this is that the VIX can stay low for extended periods of time, as equities grind higher in the absence of fear catalysts.

Notable piece from WSJ on reaching for yield down under. In-flows into Australian bonds have kept the currency strong.This phenomenon is interesting for multiple reasons:

(click to enlarge)

The source of AUDUSD strength explained. This presents a clearer picture of why the Aussie dollar short-term bottomed on July 1, 2012. Incoming capital flows buoyed the currency.

Dangerous assumptions re, China revealed. Those "reaching for yield" via Australian debt are implicitly assuming China's hard landing will not destabilize Australia's heavily natural-resource-leveraged economy (with housing bubble to go with). This could prove an exceptionally bad assumption.

Potential double negative for AUDUSD moving forward. If the global slowdown grows more serious, strongly impacting base metals prices - as others have noted, copper looks very vulnerable - then assumptions of China avoiding a hard landing could be proven false, severe decline in base metals prices could follow, and the double down Aussie carry trade could unwind in severe fashion.

On the other hand, if the "risk on" rally in Western assets appears sustainable, AUDUSD could decline anyway as foreign capital withdraws from Australian debt holdings and returns to local opportunities.

In this low conviction macro environment, we still very much like the big-picture drivers for short AUDUSD.

- China's Unlivable Cities - Foreign Policy

- The Only Way Out - Caixin Online

- China Reluctance on Reserve Cut Signals Inflation Concern

- Price War Rattles Chinese Retailers - WSJ.com

- Hot Money Turns Cold On Chinese Prospects - WSJ.com

- China's Bear Market Lures Foreign Bids as Locals Pull Funds

- Muted inflation supports more Fed easing | Reuters

- FT Alphaville » More good news. Now what?

- S&P 500 likely to be mired until options expire | Reuters

- Greece seeks two-year austerity extension - FT.com

- Greece to Exit Euro Zone Next Month?

- Economic Crisis Triggers Wave of Suicides in Greece

How crappy has forex been as a return generator these past few years? Epically crappy:

Brevan Howard, which managed $36.7 billion at the end of June, started Ding's Macro FX in 2009. The fund has produced an average annual gain of 3.6 percent since its inception in November 2009 through June of this year, compared with a 3.7 percent rise for the broader industry, according to data compiled by Bloomberg and Chicago-based Hedge Fund Research Inc.

Other hedge funds that trade currencies based on global economic trends produced an average annual loss of 0.9 percent from November 2009 through June of this year, the most recent data available from Hedge Fund Research.

- Paulson Steps Up Gold Bet to 44% of Firm's Equity Assets

- Paulson, Soros Add Gold as Price Declines Most Since 2008

Paulson, 56, has lost 23 percent so far this year in his Gold Fund and 18 percent in the Advantage Plus Fund, in part because of wrong-way bets on mining companies. Advantage Plus, which seeks to profit from corporate events such as takeovers and bankruptcies and uses leverage to amplify returns, declined 51 percent last year.It makes me want to shout, WHAT THE HELL HAPPENED TO RISK MANAGEMENT? Does Paulson somehow get a pass on risk management, just because he manages billions? And now he is "doubling down" on his gold bets… already down +20%… What is wrong with these guys? What is wrong with their investors?

More Bullish Setups

Part of our process involves scanning hundreds of charts (typically 400+), both mechanically and visually, on a daily basis. The feedback of this scan gives additional flavor as to the character and positioning of the market.

We are starting to see more bullish setups pop up now, and more winning stocks separate themselves from losing stocks. The picture is consistent with bulls gaining traction as overbought conditions resolve through time rather than price.

Notable technical developments:

- High-yield consumer staples weak. Time for rotation out?

- Utilities vulnerable? Another sector exposed to rising yields / risk rotation.

- Solar stocks possible bottom. TAN long downtrend over?

- Junk bonds resolving bearish. Shift out of high yield as well?

- Silver hanging tough. Possible refusal to break means imminent rise?

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

No comments:

Post a Comment