No doubt, but margins and revenue growth are

what the market obsesses over and near term both looking to be reversing course.

For them to refer to mobile as 'exciting' is a whole lot of bs....they are

behind the curve there and still trying to figure out how to adjust. As for

Qihoo, I doubt it amounts to much but it will be a thorn in the stock till mgmt

can show revenue growth picking back up. Also think you now have risk baidu does

a stupid acquisition....let's see. Anyway, what interest me is the share price,

and right now i expect this to be an easy name to be on the short side on till

the stock washes out or evidence to the contrary emerges.

Baidu Q3 Recap: Undergoing Transition, The Reign Is Far From Ending

Disclosure: I have no positions in any stocks mentioned, and

no plans to initiate any positions within the next 72 hours.

Key highlights:

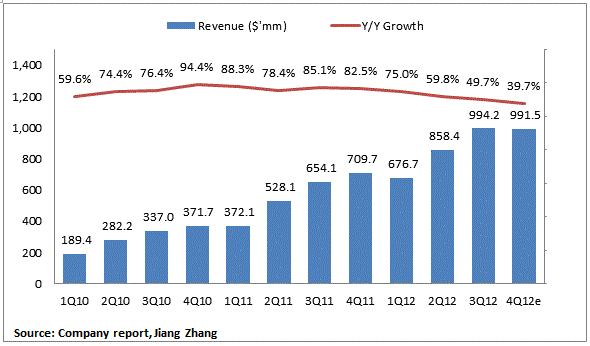

- Revenue: $994.6 million, +49.7% y/y

- Operating profit: $524.6 million, +48.1% y/y

- Diluted EPS: $1.37, +59.8% y/y

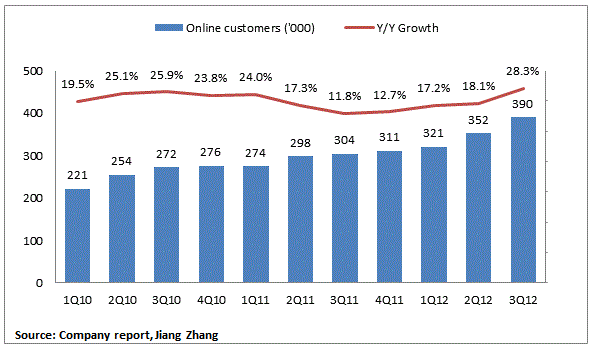

- Online revenue customers: 390K, +28.3% y/y

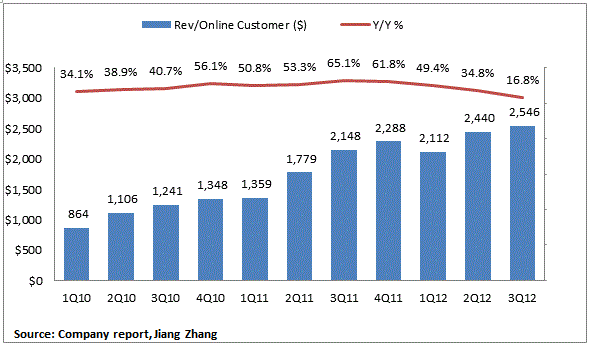

- Revenue per online marketing customer: $2,546, +16.8% y/y

Despite a combination of a macro environment that was weaker than 3Q11, growing PC to mobile shift and changes in competitive dynamics, Baidu continued to execute with an almost inline revenue growth and an EPS that beat consensus.

Customer acquisition was very robust, thanks to Baidu's experienced and efficient sales team. Total online customers reached 390K, +28.3% y/y and accelerating for the fourth consecutive quarter. Strong customer acquisition indicates that 1) Baidu is growing its customer base despite new entrants and 2) growing SME customer base lays a solid foundation for future monetization in mobile. In Q3, the top five spending customers are from medical/health care, education, travel, machinery and franchising. According to management, B2C sectors continue to grow steadily while B2B faces some headwind.

click to enlarge images

In addition, revenue per online customer climbed sequentially, +4.3% q/q, suggesting solid execution by the management.

While I note that ARPU decelerated sharply on a year-over-year basis, investors should recall that ARPU was rather strong in 3Q11 due to hot money from ecommerce and group-buy companies. Since then, these sectors have cooled down a bit and I believe that Baidu's current ARPU is growing at a more sustainable level.

What Concerned Me: Revenue Miss and Weak Guidance, Slow Mobile Transition

Baidu's revenue of $994.6 million came in below consensus of $1.0 billion. In addition, the company guided $979 million - 1.01 billion in revenue for next quarter, below the consensus of $1.03 billion.

The revenue miss and the soft guidance may be due to growing competition from Qihoo. Back in August, Qihoo introduced its own proprietary search engine that immediately captured 10% of China's search traffic market. While I do not believe that Qihoo will be a long term threat to Baidu due to Baidu's superior search technology, proven track record and better user experience, Qihoo's presence and continued investment on it search engine could weigh in on Baidu's stock in the near term.

Like its global internet peers, such as Google (GOOG) and Facebook (FB), Baidu is also experiencing fast PC-to-mobile transition of its users. According to management, mobile traffic to Baidu increased at triple digit rate in the past quarter.

Transitioning from desktop to mobile monetizing will be a challenge in which I believe Baidu can overcome. Investors should recall that Baidu is no stranger when it comes to educating its customers and assisting them making the transition from one monetization platform to another. Four years ago, despite some skepticism from the street, Baidu masterfully developed, integrated and commercialized its Phoenix Nest system, which is currently the company's hallmark monetization platform. For mobile, I believe that Baidu can also successfully execute its monetization strategy.

In my view, Baidu's 10 plus years of search experience, proven management and strong brand among users will allow the company to overcome the current mobile and competitive concerns in long run. This transition period presents an attractive opportunity for investors, given that Baidu, which trades at its historical lows and 18x 2013e earnings, is starting to look like a value play.

- Starbucks Q4 Earnings Preview: Continued Strength In K-Cups, Macro May Weigh In Fri, Oct 26

- LinkedIn Q3 Earnings Preview: Expect Solid Results, Mobile Monetization In Focus Fri, Oct 26

- Apple Q4 Earnings Recap: Mixed Results; iPad Cannibalization A Key Concern Fri, Oct 26

- Baidu Q3 Earnings Preview: Emerging Competition And Mobile In Focus Thu, Oct 25

When baidu transitioned to phoenix next they where the only real player in china and google was in the process of exiting. Coming into last quarter I was already worried about bidu growth slowing because of mobile, and clearly this quarter confirmed it. Qihoo just makes the whole thing even worse because they have showed up at an ideal time to take them on. While i think its easy to say baidu should navigate this, the risks are definitely not minor and this is assuming google doesn't consider throwing themselves back into the fold. I am short the stock and would not go near it long until I have a clearer picture on just how bad things will get before they stabilize.

User experience and relevance is what differentiates search engines. In this case, Baidu has the better search technology and will ultimately win in the search engine battle.

There is a lot to like in your analysis and Baidu's quarter. I was fearful of a weaker quarter given the constrained economic environment. Either Baidu is economically insensitive or they expertly managed their way threw it. Suspect some of both. Management guidance seems to reflect continued economic concerns. Your thoughts?