Disclosure: I have no positions in any stocks mentioned, and

no plans to initiate any positions within the next 72 hours.

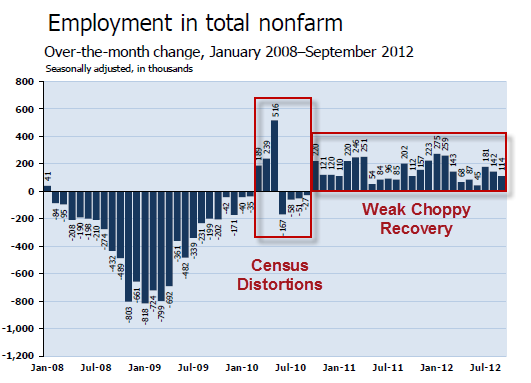

Employers added a seasonally adjusted 114,000 jobs, a tepid pace that was accompanied by data revisions boosting the number of positions added in previous months by 86,000. The new figures showed that the nation added 181,000 jobs in July and 142,000 jobs in August, and that third-quarter job growth was far higher than in the spring.The charts below, from Doug Short, illustrate why the consumer side of the U.S. economy is going nowhere.

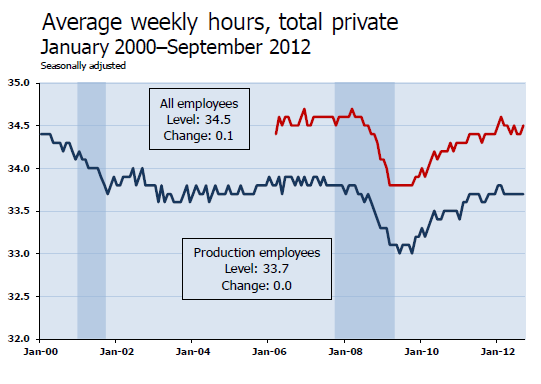

Still, part of the growth came from a surge in the number of people taking part-time jobs because full-time slots weren't available. Of the 104,000 new private-sector jobs, the bulk came in health care, which added 44,000, and transportation and warehousing. Manufacturing employment fell by 16,000. (WSJ)

(click to enlarge)

'

(click to enlarge)

'

(click to enlarge) (click to enlarge)

(click to enlarge)

Education Matters

(click to enlarge)

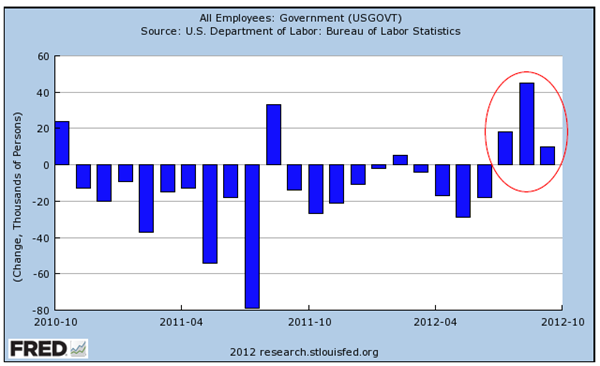

Of the 114,000 new jobs, 104,000 were in the private sector. Yet, all of

the 86,000 in upward revisions for July and August came in government

jobs.

Of the 114,000 new jobs, 104,000 were in the private sector. Yet, all of

the 86,000 in upward revisions for July and August came in government

jobs.- Governments have been cutting jobs almost every month since November 2010 but went on a hiring spree lately. Since July, governments have added 73k jobs after laying off 65k employees between January and June. Hmmm…

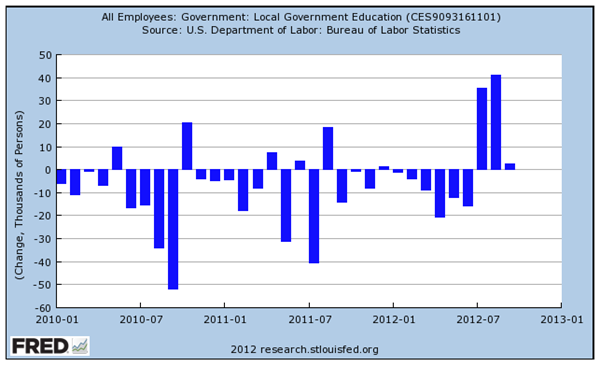

- State and local governments have suddenly decided to boost their educational employees: over the past 3 months, state and local education-related jobs have swelled by 23k for state and 79k for local governments. For the latter, the last 3 months' new jobs are only 4k shy of the total job losses of the previous 9 months. Hmmm…

- Excluding state and local education, governments have continued to cut employment at an average rate of 10k per month.

- Manufacturing employment fell again (down 38,000 in the last two months).

- The number of part-time workers for economic reasons grew to 8.6 million in September from 7.7 million in March. Part-Time Work Can't Support Full-Time Spending

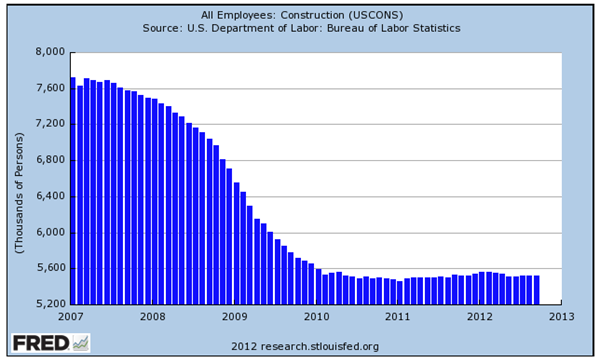

Meanwhile, the all important construction sector remains stagnant:

(click to enlarge)

INTERESTING VIEWPOINT:

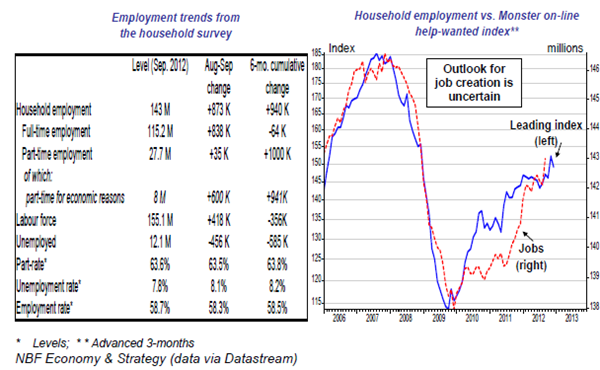

The September jobs report shocked many due to the big decline in the unemployment rate. Given the ongoing debate about the "quality" of the numbers, we think that a few clarifications are warranted. First, the jobless rate is calculated from the household survey, not the payroll(click to enlarge)

survey.

This a methodology similar to that used in Canada to report jobs. Canadians are accustomed to the inherent volatility of such surveys and as such, it is customary for us to look at changes over a 6-month period to really gauge the underlying trends in labour markets (that's what the Bank of Canada does). So what is the situation in the U.S.?

As today's Hot Chart shows, the U.S created 838K full-time jobs in September but the cumulative 6-month change is still showing a loss of 64K (part-time jobs are up a million over the period). The labour force showed a large increase of 418K jobs on the month, but we are still down 356K since March. The part rate, employment rate are also not that much different than they were last spring.

The bottom-line is that the good performance in September does not change the fact that the trend remains uninspiring over the past six months. What's more, the outlook is not that great. As shown, the Monster on-line jobs index (a leading indicator) recorded its biggest drop since October 2010 this month. This points to a rising jobless rate.

In all, my "educated" guess is that the October report will not be so good and that the basic slow trend remains.

The YoY growth rate in employment is still 1.4%, but monthly trends continue to point to a slowdown to 1.2%. Combined with slow wage growth and inflation stuck in the 1.5-2.5% range, consumer spending will likely remain weak well into 2013.

Domestic earnings will be harder to come by during 2013 while the rest of the world will continue to struggle.

Equity markets are very cheap at present, but a slowing U.S. economy will add to investors' angst about Europe and China, keeping equities undervalued for a while longer (PE's, QEs and Saudis). Prudence remains paramount.

No comments:

Post a Comment