- Theta said...

- How much of this underperformance of banks compared to broad indices is alpha and how much beta?

- January 29, 2016 at 9:01 AM

- Anonymous said...

- Can always rely on the BOJ to double down when it comes to weakening the Yen and bidding equities.

- January 29, 2016 at 9:10 AM

- Eddie said...

- Abee,

I think we are on the same page here. The only difference is that I prefer to think in terms of yield (equities' duration is much longer than that of the long bond... so I have nothing to compare against... there goes the Fed model btw). To me equities are basically perpetual deeply subordinated bonds which means lower price equals higher yield and vice versa.

Historically US equities yielded around 6% capital gain per year and around 3% dividends. So I think equties are "fairly" valued if the return over a reasonable time frame (10 years in my world) is around 9%. The difference between you and Siegel is that the latter says equities are always a buy, but tacitly ignores time. If you bought the S&P around mid of 2000 you should sit on a return between 0% and treasury yields until now...

Regarding "timing" I think it reasonable to wait for prices that give me the yield I want. Which means something between 950 (Hussman) and 1120 (Grantham) in the S&P. And I fully expect to see those over the course of this cycle. This wouldn't be bargain prices, btw, just "normal" valuations.

For the record, I am net long, with some single names that should prevail imo, some bombed out ETFs *cough*GDX*cough* and a healthy portion of cash and index shorts.

Re DB: I heard that morale was already low before the whole Russia business and the latest figures. They are too big to fail imo but you won't hold the bag... eehh... stock though. There should be at least one more capital increase. Regading banks I prefer WFC or JPM. - January 29, 2016 at 9:51 AM

- Eddie said...

- MacroMan,

may I ask what your definition of "orthodox market correction" is? - January 29, 2016 at 10:13 AM

- Anonymous said...

- Japan is blatantly engaging in currency war tactics with the US. Debasing their currency they seek to drive up the USD, destroying the earnings of American companies. We need to impose tariffs and trade barriers on Japan - hopefully China will do like wise.

- January 29, 2016 at 10:19 AM

- Theta said...

- Eddie,

Here's an argument for equities having a lower duration than the long bond:

http://www.jstor.org/stable/4479256?seq=1#page_scan_tab_contents - January 29, 2016 at 10:20 AM

- rossco said...

- even by recent standards the price action in the Nikkei today was beyond ridiculous

the weakening dollar theme has been well and truly nipped in the bud

who is next in the Asian currency race to the bottom ? - January 29, 2016 at 10:23 AM

- TheBondStrategist said...

- When they ever understand that NIRP will kill banks and money velocity?

rates are out of control... dangerous times ahead i suppose...

I hope markets will show them what they're doing... - January 29, 2016 at 10:44 AM

- Anonymous said...

- Algos/HFT are destroying capital markets with this insane volatility. There needs to be a tax on HFT.

- January 29, 2016 at 10:48 AM

- TheBondStrategist said...

- Algos/hft means nothing in a medium term picture...

there's only a way to stop this asset deflation.. a G20 statement when they agree that race to bottom in rates is finished and won't be there any more unilateral FX depreciation...

wonderland?? do we really need a bank collapse before?? probably - January 29, 2016 at 10:54 AM

- Macro Man said...

- Eddie, you estimate of long term returns for the equity market are way, way overcooked. I believe the long term returns are closer to 6-6.5% than the 9% that you suggest.

For me, an orthodox market correction is a drawdown of less than 20% that does not accompany a recession. - January 29, 2016 at 11:06 AM

- Eddie said...

- Theta,

thanks for the link. Two things bother me, though.

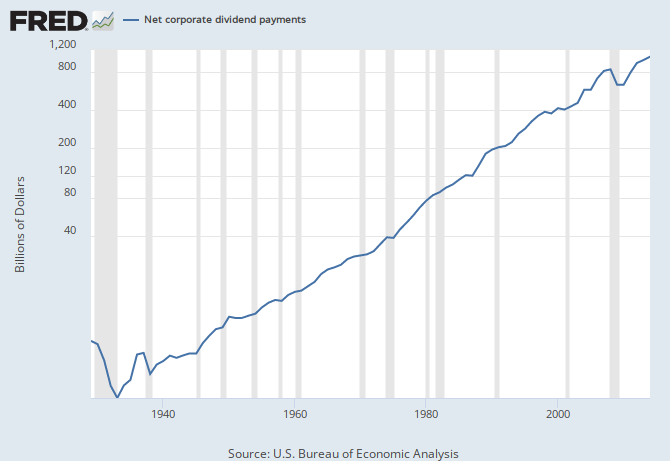

The assumption that increases in inflation flow through to the net income, at least to a significant extent (the authors claim 80%) sounds unrealistic to me. We are not talking about retail or tech companies, for sure. Utilities might fit the bill. These companies would be fantastic investments, anyway. Also the value of 80% was measured during the period from 1980 to 1987 (footnote 7), which is not very representative imo.

They claim that dividend growth is highly volatile. Since their chart doesn't show much I consulted FRED and got this (left hand scale is logarithmic):

FRED: Net corporate dividend payments.

It's not a perfect straight line, especially not during 2008/2009, but for me that's good enough. I think I will stick to the Dividend Discount Model for the time being :). - January 29, 2016 at 11:08 AM

- Macro Man said...

- @TBS: "Asset defaltion" is exactly what we do not have; to the contrary, we've had rampant asset price inflation as CBs have enoucouraged/forced investors to move out the risk curve over the last six years.

Given the degree of overcapacity in the world, it strikes me that there is little hope to independently stoke inflation until either capacity goes permanently off line or global consumption catches up to supply. I'd remind readers that this situation is actually not anomalous from an historical perspective. - January 29, 2016 at 11:10 AM

- TheBondStrategist said...

- Asset reflation is finished some time ago.... and pay attention, isn't universal.. there's only one asset reflation that has universally worked, and it's due to zirp and lower for longer (FI rates on freefall): govies and asset priced on FI rates..

are you seeing asset reflation on EM? on real assets? on equities?

house prices are not moving in same ways everywhere.. and differently on the same country...

Asset reflation is potentially a mixed concept... not played in the same way for Facebook and FreeportMcmoran. - January 29, 2016 at 11:28 AM

- Eddie said...

- MacroMan,

I look at Shiller's data for the S&P (actual and implied) which can be found here.

If I look at the S&P price in Jan 1949 (I dunno how long I can go back due to data quality issues...) and at the price at Jan 2009 or Dec 2015, doesn't matter, I get a CAGR of more than 7%. This excludes dividends.

Where do your figures come from? - January 29, 2016 at 11:28 AM

- Macro Man said...

- Eddie, looking at the whole dataset from 1871, I see average annual price gains of 4.4% and an average dividend yield of 2.22%, rendering a total return of 6.62%.

- January 29, 2016 at 11:37 AM

- Booger said...

- The BOJ ceases to amaze me.

It is hard to be a USD.JPY bear in a bear cave with the BOJ when they still have a gun. Ok, they have fewer bullets, but it's hard to count exactly and you just never know when they will be nuts enough to let one off. Now the logical thing to do for the BOJ if they had only 3-4 bullets left is to wait until a real crisis, or when the bears are real close. So maybe they have more bullets than we realize or maybe they are just crazy in letting off another one yesterday, when really there was no reason to.

No point waiting for the BOJ to misfire or miss, I think you have to wait for them to run out of bullets for a decent position shorting USD.JPY and then the bears will be all over them. Now that will be an interesting thing to see. - January 29, 2016 at 11:49 AM

- Anonymous said...

- Switzerland voting to end fractional reserve banking:

http://www.businessinsider.com/switzerland-might-end-fractional-reserve-banking-2016-1 - January 29, 2016 at 11:53 AM

- Anonymous said...

- TheBondStrategist - You need to do some basic research. MM is correct, there has been MASSIVE asset inflation in equities and real estate almost everywhere. Check every equities chart. Check property prices in every major city.

- January 29, 2016 at 11:56 AM

- Anonymous said...

- Booger - Yes the BOJ are the biggest manipulators of financial markets in the world. Let's hope Kyle Bass' thesis on Japan works out and those b*stards go bust.

- January 29, 2016 at 11:57 AM

- abee crombie said...

- Nice post MM. Financials are a screaming buy here, IMO. Go through and read the calls on citi or JPM, these guys don't have so much oil and gas exposure and although the market got spooked, even if oil stays at $30 the losses to capital are pretty insignificant .. Perhaps the market was more spooked by the reduction in fed hikes and 10 year rates which the big US banks need to earn NIM, but banks are trading well below book value, and unless we get a recession don't have a lot of upside priced in.

And you can look across the financial space, it's not just big banks, mReits, leasing companies, asset management. Etc etc. if you bought banks in 2011 you doubled your money pretty quick. I think a similar situation is shaping up. For those more macro in mind, when the banks start out performing I think it's a good risk sign. And I am basing most of my argument on US financials. - January 29, 2016 at 12:03 PM

- Bruce in Tennessee said...

- http://www.marketwatch.com/story/heres-one-argument-why-china-will-lose-its-currency-war-2016-01-28

The problem, however, is that China’s competitors are employing the same tactics and their currencies have more or less shadowed the yuan’s movements against the dollar, according to Englander.

“If the trading partners keep matching CNY depreciation at this pace, CNY will have to go a long way before any material competitive advantage emerges,” he said.

That has not deterred the Chinese authorities from pushing the currency lower after its dramatic devaluation in August and analysts project the yuan-dollar pair USDCNY, +0.0806% to soften to 7 by the end of the year from 6.57 currently.

Ironically, in a bid to buttress the economy via the cheap yuan, China faces the risk of accelerating capital outflows.

...The graph shows that USD is moving up against all of Asia....not just China, as noted by the article... - January 29, 2016 at 12:05 PM

- TheBondStrategist said...

- Guys, i haven't told that asset reflation hasn't happened... i'm telling that it isn't working anymore and everywhere...

my simple view is that from 3+% to zero you can reflate.. from zero to -infinite doens't work in the same way..

"Check every equities chart. Check property prices in every major city." Please stop looking at s&p500 and London prime prices...world is bigger than you think... - January 29, 2016 at 12:08 PM

- washedup said...

- @abee - I will stick to mREITs because I like the prospects of negative interest rates getting them a positive carry on both legs. That and the fact that I enjoy being mercilessly flogged and humiliated.

On a more serious note, I think banks may have further increases in regulatory scrutiny with the political climate and banking fees have probably peaked for the cycle, which rules out most of the big boys. I can't find too much wrong with a WFC or regionals though - household formation is strong and when you tune out the noise that matters the most for a domestically focused bank. - January 29, 2016 at 12:09 PM

- Bruce in Tennessee said...

- http://www.wsj.com/articles/u-s-durable-orders-fall-sharply-in-december-1453988247

“Industries faced stiff competition from foreign rivals for U.S. market share, and exporters faced intense pressures abroad.” Thursday’s release is in line with data from Institute for Supply Management, a group of purchasing managers, showing a nearly three-year-long expansion in manufacturing came to an end in November. And the Federal Reserve’s reading on industrial production has declined in 10 of the past 12 months, putting it off nearly 2% from its peak in December 2014. A number of forces hampered U.S. factories last year. An economic slowdown in China, Brazil and other markets for U.S. goods limited foreign demand. Meanwhile, a stronger dollar made U.S. goods more expensive overseas and foreign products relatively more affordable for American consumers. And a pullback in U.S. oil production last year reversed a recent source of strength for many metal and equipment makers."

...When paired with the previous post, in that China isn't getting the competitive jump it expected because all their trading partners are copying their moves, it appears our manufacturing bust will continue, as the dollar should get stronger and durable goods should continue to weaken...

2 cnets... - January 29, 2016 at 12:12 PM

- Eddie said...

- Touche MacroMan. This is where the data quality issue comes into play. I know that earlier part of the series has been reconstructed, but I don't know off the top of my head until when. So I was hesitant to go back the full way.

- January 29, 2016 at 12:21 PM

- Anonymous said...

- TBS - Go buy a house in Vancover, Sydney, Singapore, Dubai... then come back and tell me there isn't a global property bubble. We're talking asset price increases of 100's of % and valuations of 10x earnings or more. It's not just London.

- January 29, 2016 at 12:25 PM

- Martin T. said...

- "For those more macro in mind, when the banks start out performing I think it's a good risk sign. And I am basing most of my argument on US financials."

Dear Abee Crombie,

For me a bank is the second derivative of an economy. If you think US growth is going to accelerate, then it makes sense to play the "beta" game. I don't see US growth accelerating? Do you?

Also, Banks’ net interest margin is already at the lowest level in history (check FRED...).

Underperformance by the banking sector always is a bad sign for markets and the economy; it suggests that the credit mechanism is clogged, with knock-on effects for the rest of the economy.

The flattening of the yield curve have left the banks with sharply reduced earning potential. The banks invest more in Treasury securities than in business loans, and the flattening yield curve crushes the differential between their cost of funds and the yield they earn on Treasuries. How is that going to make their business "profitable"?

So sure, go ahead, go for Financials, go for your "screaming buy".

Best,

Martin - January 29, 2016 at 12:55 PM

- Leftback said...

- Let's conclude the debate on asset prices by saying it's patchy - there is no doubt that global real estate dirty money laundering hot spots exist all over the world - and you can add Manhattan and San Francisco to that list. Now go look in the Midwest or Pennsylvania and you'll see a moribund housing market wherever regional employment is especially weak.

If you want to talk equities, there is (arguably) generational value and low price available in Brazil and Russia, which are "out of fashion", while Spoos and Nikkei both seem a little rich, with Shanghai clearly not done wringing out the last drips of speculative excess from the recent bubble. So it's all very patchy and simply represents the envelope of places the super-rich are dropping off little wads of money in an effort to avoid taxation.

B in T, LB is still long equities, and be aware that this trade is grinding out some gains for us. However, we are open to the idea that this is now a bear market where we sell the rips instead of buying the dips. It's just that the data are not quite 100% conclusive, although to us the chart of the R2000 makes a pretty convincing argument. Macro-wise our biggest and most reasonable fear is another bout of devaluation from PBoC, and indeed we think that comes later on in the year.

Still we have all been wrong before. We are keeping an open mind and watching what develops. The trading strategy for now is to stay long until volatility ebbs and the news flow becomes complacent or "happy-clappy", in the phrase that is preferred here on the blog, luring the unwary in to the market to buy assets at prices where we would rather be offering than bidding.

We bought XLE and BP calls back in the sub-$30 oil abyss, btw, and that's doing nicely. It's just a trade, not an existential statement of philosophy, B in T, btw. We are agonistic about many markets, other than rates, where it is lower for longer. Above all else, I want to stress to B in T that being right is fun, but it just isn't as important right now as making money, or at other points in time, as preserving money in the way that you have also succeeded in doing. - January 29, 2016 at 12:59 PM

- TBc said...

- Anyone have a sense of why the CNH/CNY spread is tanking?

The cynic in me says there's a new policy coming over the weekend - January 29, 2016 at 1:12 PM

- Anonymous said...

- EUropean equities are not liking the increasingly negative rates. As bund etc goes bid, dax etc omces off.

Equities are possibly about to send a signal on negative rates.

How does that work for Draghi in March?

We will possibly look back at this era of negative rates as the most ill-conceived of all Central Bank policy. And that's saying a lot! - January 29, 2016 at 1:16 PM

- Anonymous said...

- Also, 8 days ago Kuroda said was not even contemplating Neg Rates.

What changed? - January 29, 2016 at 1:19 PM

- Macro Man said...

- @TBc, I think the authorities have been intervening pretty heavily in both to keep the levels where they want 'em. Heard estimates approaching $200 bio for the month.

@Anon 1.16: I wrote this on Twitter early this morning: Amazing, really, that charging people for holding money is now seen as monetary stimulus. In fiscal terms that's called a 'wealth tax'. I see that something like 57% of German bonds eligible for QE are trading negative, with more than a third trading below the ECB depo rate. How's that for NIM? Judging by the charts above, 'pretty lousy' is the answer. - January 29, 2016 at 1:20 PM

- Bruce in Tennessee said...

- Lefty,

No need to get sensitive. This blog allows debate about ideas. Only profit and loss are the judges, and I am sure you are making money.

I have noticed that you tend to post more and get shriller if your trades are going south...we all do this to some degree. You boys do this for a living, and that's grand. Frankly, I don't think doing this full time would have appealed to me.

And I don't understand today's global financial players. It seems to me that Japan's initiation of NIRP-lite that everyone is discussing is going to be bad in the long run for US manufacturing and of course exporting. Yet our futures are up today, and probably we will finish green. When you boil it all down, though, it seems that just as the world followed QE, that in the end we will all have to go down the NIRP road too. Just seems logical....There is of course the old bugger bear...tariffs...that could be instituted across the board if anyone who cannot stand equities (for instance the elderly) would ever like a ROI...there will come a time when all the old people who own their homes have cashed out with negative mortgages and with NIRP...it might just be Solyent Green time... - January 29, 2016 at 1:27 PM

- EuropeanBull said...

- @MMM & Eddie:

you both are right somewhat. There is a structural break in this data set between the 30s and the 50s and is characterized by the monetary regime, as deflation was a regular visitor before. If you look at the data in real terms (Shiller is so nice to supply the series in the same sheet) the long term trend is more stable! - January 29, 2016 at 1:30 PM

- Anonymous said...

- Guys, please see this (NIRP) situation from the point-of-view of desperate central banks and bankrupt governments. I have and furthermore, I've decided to be patriotic and act decisively to assist them. Starting Monday I will allow any, and all, institutions to send me unlimited quantities of money, and to assist them further I will charge them for this. To get the "best deal" I suggest they deposit said funds with me for a duration period exceeding my lifetime. If things get desperate and they wish to cancel some of their debt, and thus have me re-balance their holdings by not returning some funds I can also arrange for that to happen.

Finally please note that this offer is open to sovereigns, central banks, banking institutions and also to you dear readers. Really in such difficult times it's the least I can do. - January 29, 2016 at 1:34 PM

- Macro Man said...

- @EB, yes it was the 1950's where equities became "permanently" more expensive. Taking a step back, however, I don't think it is feasible to expect equity returns to outstrip nominal GDP (or domicile-of-sales weighted nominal GDP) ad infinitum.

- January 29, 2016 at 1:35 PM

- TheBondStrategist said...

- LB successfully summarized my thinking... Asset reflation has workED, not everywhere and not in the same way.. Let's try Rome, Seville, Cairo..etc..

Is there a property bubble around? yes, but localized... and being an illiquid asset, i think we'll see some downside (in London prime market you're seeing that..)

MM, so we agree, negative rates are a tax on wealth. No stimulus, only a recipe for deflation... trasmission channels are rates and banks...

EurChf going parabolic... any insight? - January 29, 2016 at 1:38 PM

- Confused said...

- NIRP = a bid in treasuries and USD, this will remove liquidity for US equities.

Furthermore the PBoC and now BOJ devaluations will push up the USD, hurting US corp earnings, which will hurt US equities.

Imposing tariffs on the banking sector and pushing them to taking on more risky loans (via NIRP) will hurt financials, thus hurting equities.

Please tell me how equities will rally here? - January 29, 2016 at 1:42 PM

- Anonymous said...

- EURCHF is likely SNB intervention. There were rumors of this a few days ago.

- January 29, 2016 at 1:43 PM

- EuropeanBull said...

- @MM:

agreed. Are you sure that returns have outperformed the domicile-of-sales weighted nominal GDP? I am not, or at least have never seen a trustworthy analysis.

That said, US equities still are far from a bargain and do suggest below trend-returns for the next 5-10 years. Whether this will unravel in a crash as the ZH community believes or in couple more years like the last one will depend on the economic cycle. - January 29, 2016 at 1:45 PM

- Anonymous said...

- @12:25

no real estate bubble in Dubai, that's for sure.

Prices here are tanking since a mini bubble in 2013/14.

Down easily 10-15% from that peak and new villa's and apartments coming on the

market in the thousands............and no buyers in sight.

And the local currency (Dirham) peg to US$ makes it too expensive for many foreigners who's currency is tanking as well......so double trouble. - January 29, 2016 at 1:52 PM

- abee crombie said...

- Martin T...perhaps screaming buy is too hard of a term. But I do think US Financials are very undervalued. Can the world be tipping into global recession and thus Financials are really expensive, I guess. We can each decide on those probabilities.

The problem with financial markets is that everyone is looking at the here and now and not many pay attention to the longer term. And in the long term valuation plays a significant role in your returns.

The problem with QE and the world we live in is that it inflates some asset values and then deflates them when the fundamentals catch up (over capacity). But all assets (in general) have a fair price band. When markets move prices below a fair price, even if the near term trends are deteriorating it makes sense to start buying bc the world is still awash with money. And money needs to earn a return eventually (after it is done hiding). When US housing was trading below replacement cost, foreigners and cash buyers came in. Similar with equity markets post GFC. Time will tell if I am right on financials being under valued... - January 29, 2016 at 1:56 PM

- Bruce in Tennessee said...

- But all assets (in general) have a fair price band.

...Probably true at ZIRP or NIRP...but this road is like hobbits going into a mountain in the dark....IF we leave today's stimulus, what happens to assets? Does time produce a persistent brake to these policies? - January 29, 2016 at 2:03 PM

- algoman said...

- I'm expecting a move up in equities on the US session. Buy algos are coming onlibe.

- January 29, 2016 at 2:06 PM

- washedup said...

- MM - if you repeated your survey from a few days ago I think you would reach a different conclusion - I don't know what changed (equities are more or less where they were), but I haven't seen risk sentiment this negative on the board since q4 2008.

Abee I think US exposed financials are a safe, staid, utility stocks at this point (DB notwithstanding!) - they will keep trading at a discount to BV and sneakily increase dividends over time, so total returns will be good, but I doubt they will double or triple anytime this decade. I don't see more than 20% downside either (a distance AMZN seemingly covers in a day!) - January 29, 2016 at 2:07 PM

- abee crombie said...

- Just following up on my previous thought. Another big problem with the markets today is Hedge Funds are the marginal players in most stocks. And what most hedge funds dont do is catch a falling knife. They all want to get the "turn" when fundamentals have bottomed and then some good news comes. So in the meantime, when stock prices fall, there is very little "valuation floor" bc its just too dangerous to stick your neck out. Add to that a lot of value traps created by technology and overcapacity issues that most value guys didnt see mean even most value guys need a bigger discount to "margin of safety" than before. And that is not even including all the trend following monkeys that seem to drive markets anyways

How it all works out is anyone's guess, but like Graham/Buffet said, in the short term markets are a voting machine, in the LT they are a weighing machine.

BiT. I am worried about ZIRP but I see the bigger worry as inflation vs deflation. Asset prices will just fall to a point where valuations get too cheap to ignore in a worst case scenario, and CB's will keep on printing. As BoJ showed, they are pot committed and dont have any other options. I expect the inflation to emerge when policy makers realize they should have used fiscal stimulus vs monetary stimulus and that unleashes inflation - January 29, 2016 at 2:25 PM

- Bruce in Tennessee said...

- Well, abee, truth is, and we all recognize it, is that the Fed wasted all these years of...well non-recession by keeping interest rates at zero. But if they hadn't had zero rates, well, we wouldn't have had non-recession, you argue? Yes, I see the circular trend in that...you realize that Joesph Heller was ahead of his time:

"You mean there's a catch?"

"Sure there's a catch," Doc Daneeka replied. "Catch-22. Anyone who wants to get out of combat duty isn't really crazy."

There was only one catch and that was Catch-22, which specified that a concern for one's own safety in the face of dangers that were real and immediate was the process of a rational mind. Orr was crazy and could be grounded. All he had to do was ask; and as soon as he did, he would no longer be crazy and would have to fly more missions. Orr would be crazy to fly more missions and sane if he didn't, but if he was sane, he had to fly them. If he flew them, he was crazy and didn't have to; but if he didn't want to, he was sane and had to. Yossarian was moved very deeply by the absolute simplicity of this clause of Catch-22 and let out a respectful whistle. - January 29, 2016 at 2:33 PM

- algoman said...

- Are you liking my equities rally?

- January 29, 2016 at 2:51 PM

- algoman said...

- This is an example of seeing Central Bank algos ahead of time.

- January 29, 2016 at 2:53 PM

- Eddie said...

- Re CNY: GS guesstimates that %185bn have been spent on intervention during Jan.

- January 29, 2016 at 3:06 PM

- washedup said...

- No - this is an example if back trading.

- January 29, 2016 at 3:06 PM

- CV said...

- Not exactly a fun end of month for Mr. Shorty here. The ECB and the BOJ have done their part to get the chase going. Let us see whether seasonals/rebalancing will too.

Of course, comments like "buy algos are coming online" always make me wary, but we did have the Economist do "an explainer" on a bear market a few days ago, so I reckon the pendulum can still swing further!

Now, on EZ banks. Look there are many stories here which easily get confused. The BRRD (banking recovery and resolution) directive has shaken things up because it basically means that SMALLER banks' equity and credit are hanging in the balance. Governments and the ECB will screw these people like they did in Novo Banco; more crazy stuff ahead! Meanwhile, the bigger banks are more difficult and the case of the poor MPS is a great example. Also the new "bad bank" in Italy shows us that you can always count on a diabolical fudge when there is just a remote "systemic" risk.

In the medium/long term, a current account surplus, QE and ZIRP will contribute to the zombification of some EZ banks but ALSO, arguably, allow some to prosper. It's all part of the plan you see ... the ABSENCE of crisis in the Eurozone remains a powerful sedative, and should not be ignored.

If all three of these tailwinds were removed tomorrow, we would be straight back to 2012 in a heart beat, but it won't happen. Playing EZ banks now means being smart on BOTH the long and short side. No easy plays here. - January 29, 2016 at 3:06 PM

- abee crombie said...

- Back to trading, could we be breaking the pincers in Russell 2000, Nasdaq triangle, SPX today?

I never trust end of month rally until after 2pm. Too many wipsaws historically. But that Chicago PMI was nice! - January 29, 2016 at 3:09 PM

- Eddie said...

- Taking a step back, however, I don't think it is feasible to expect equity returns to outstrip nominal GDP (or domicile-of-sales weighted nominal GDP) ad infinitum.

FRED says that nominal GDP grew at a CAGR of 6.49% between Jan 1947 and Oct 2015. - January 29, 2016 at 3:11 PM

- CV said...

- "I never trust end of month rally until after 2pm

Very fair point. I suppose today's upside will then just be dumped on Monday? Not sure how the flows normally work here.

Anyway, agree with the technical points, which fits my base case. "Sell the rip" might be the theme of choice now, but you know, that requires a rip! ;) - January 29, 2016 at 3:11 PM

- algoman said...

- "No - this is an example if back trading."

"comments like "buy algos are coming online" always make me wary"

Well, 200+ ticks on NQ and climbing. Was there for the taking... - January 29, 2016 at 3:13 PM

- Macro Man said...

- "FRED says that nominal GDP grew at a CAGR of 6.49% between Jan 1947 and Oct 2015."....a period that ended with equity valuations, margins, and profits as a % of GDP all near historic highs. (Hint: these are mean reverting series.) Moreover, the prospect of long term NGDP growth at 6.5% is currently looking fairly dim.

- January 29, 2016 at 3:23 PM

- TheBondStrategist said...

- DB and Thyssenkrupp: no need to increase capital... last famous words

- January 29, 2016 at 4:01 PM

- Anonymous said...

- Are China and India both cooking their numbers?

"With a marginal expansion in manufacturing, the growth figures of 7-8 per cent are absolutely not credible," said noted economist Ashok Desai, who was part of the Prime Minister's Economic Advisory Council in the first few years of liberalisation (1991-93).

http://www.sify.com/finance/raghuram-rajan-questions-govt-s-new-gdp-formula-news-economy-qb3pE7ejbgacj.html

"http://www.businessinsider.com/chinas-statistician-being-investigated-2016-1?utm_source=feedburner&utm_medium=referral - January 29, 2016 at 4:01 PM

- Anonymous said...

- Negative rates (wealth tax), currency wars, sanctions on major trade partners (Europe on Russia & Iran to extent, distort markets from "true value", destroy a whole region with "freedom" i.e. MENA.

How does all that improve "growth & stability"? - January 29, 2016 at 4:04 PM

- Eddie said...

- ....a period that ended with equity valuations, margins, and profits as a % of GDP all near historic highs. (Hint: these are mean reverting series.)

Truer words have rarely been spoken, but this is not relevant since we were talking about GDP growth and not about growth in equity value. If we can agree that equities prices should rise around the rate of nominal GDP growth we just need to throw in 2.5 - 3% dividend yield to get to 9 - 9.5% total return.

Moreover, the prospect of long term NGDP growth at 6.5% is currently looking fairly dim.

If history is any guide (see Reinhart & Rogoff for more details) economic growth is subdued for 10 - 15 years after a housing bubble burst. Which we had... I personally expect 5 or so more years of low growth and a return to the good ol' 6.5% afterwards. We can agree to disagree here if you say that it's different this time.

Either way, thanks for taking your time to thrash this out. - January 29, 2016 at 4:24 PM

- Anonymous said...

- Thank you guys for all the great comments.

Now my point on BOJ's action is if the negative rate cannot push USDJPY above the the previous high , then that really says something sbout BOJ's ammunation. In that sense, I think B in T is right: CBs' tricks have lost its appeal and market is more and more ignoring CBs' actions.

So I see BOJ's surprising action last night as a desperate move aiming at PBOC and it is a setup for a huge short for USDJPY. I will give it three weeks to reach a peak for USDJPY and then maybe short it from there. - January 29, 2016 at 4:25 PM

- Anonymous said...

- Also, if with ECB and BOJ's shots in the arm and SPOO could not recover 50% of the loss from the end of December 2015, then it says something abou this market.

- January 29, 2016 at 4:29 PM

- Leftback said...

- B in T said:

"Lefty, No need to get sensitive. This blog allows debate about ideas. Only profit and loss are the judges, and I am sure you are making money. I have noticed that you tend to post more and get shriller if your trades are going south..."

This is neither true nor fair. We post pretty much the same frequency every day here, and in fact we usually get shriller only when Mr Shorty is bending over for the Anonymous Proctologist or people are picking up pennies in front of steamrollers.....

Somewhere, The Ghost Of Funny Money is laughing. Btw, to those who mocked the concpt of face rippers: how's yer face? - January 29, 2016 at 6:08 PM

- algoman said...

- Taken profits on equities at +2% for the day.

- January 29, 2016 at 6:33 PM

- Anonymous said...

- USDJPY rallying again, Oil rallying, equities rallying...

There is NO central bank buying... yes ofc... LOL - January 29, 2016 at 6:45 PM

- Macro Man said...

- Are they buying eurodollars too? They are up. So central banks only buy when the market is down, according to the evidence...except that they also buy every time the market goes up? LOL indeed.

"RANDOM PUNTER USES BOG....CENTRAL BANK WIPES ARSE FOR HIM" - January 29, 2016 at 6:48 PM

- The Ghost of Funny Money's Ghost said...

- I like making money off sad Knobs.

- January 29, 2016 at 6:49 PM

- Leftback said...

- Too funny, MM. The job's not done until the paperwork is complete. No idea about Central bank buying but I think Mr Shorty is probably buying today.... Cold Steel's been away, but he's back, and so are Vol Sellers. Options evisceration season returns.

- January 29, 2016 at 6:54 PM

- Anonymous said...

- Everyone is making money now, so what? My trade from 1856 is making money, shorty's trade from 2070 is making money.

Any point of making that statement? Did CBs buy shorts at 2070 and buy longs at 1856?

From http://acrossthecurve.com/

"Will negative rates dissuade an ageing population with inadequate pension and healthcare cover from saving?er… No. Will negative rates encourage investors to shift out of bank accounts and into higher-earning assets? Perhaps, but this is asking them to do what they already do. The yen already weakens in risk-on markets and only rallies when a scary world encourages capital repatriation. Does the housewife who recently got stopped out of a short yen, long Brazilian real trade really need negative rates to lend more money to Rousseff and co? Of course not! She needs something to give her confidence in Brazil, not another reason not to keep her cash at home."

So true, BOJ just attracts more shorty and expose its vulnerable nature. - January 29, 2016 at 6:58 PM

- Bruce in Tennessee said...

- Well, Lefty, we just disagree on your posts, but that makes a discussion...and as you've already probably guessed I got stopped out of SDS...as someone here once said, doesn't make me wrong, but it certainly makes me early.

Inflection point? Not yet... - January 29, 2016 at 7:35 PM

- Anonymous said...

- Central banks will run the S&P back up to 2015 highs.

- January 29, 2016 at 8:53 PM

- Leftback said...

- We took some profits today, it would have been rude (and greedy) not to. Certainly we are not bearish for the time being, but we are a tiny bit more cautious going into next week, and the risk/reward ratio has shifted to some extent.

Today would be the closest thing we have had to a face-ripper so far and it's usually not a bad time to lighten up a bit. Have a great w/e punters. Our BP and XLE options trades are buying dinner for LB this weekend. - January 29, 2016 at 9:01 PM

- washedup said...

- oh snap - no more ramen noodles for LB - a barrel of oil can suddenly get one a side salad along side a main course of halibut - don't order any wine though - that would be asking for it.

Good weekend everyone. - January 29, 2016 at 9:11 PM

- Anonymous said...

- http://www.zerohedge.com/news/2016-01-29/wtf-just-happened-here

- January 29, 2016 at 9:16 PM

- Anonymous said...

- Reuters reporting a leak from Davos, quoting Kuroda as having got the NIRP idea from Draghi and saying "...when stocks are falling this much, it's hard to justify not acting...".

So there we have it - stocks are dropping, so central banks must intervene. - January 29, 2016 at 9:24 PM

- Anonymous said...

- That Kuroda quote is one for the ages ...

- January 29, 2016 at 9:29 PM

- Macro Man said...

- Eddie...as a coda to the discussion above, I just ran the numbers on MSCI World total return, which has data going back to end-87. Annualized CAGR of....6.5%!

- January 29, 2016 at 9:49 PM

- Macro Man said...

- Re: WTF...it's almost like there might be a large monthly rebalancing or somefink...

- January 29, 2016 at 9:52 PM

- TheBondStrategist said...

- Nice short squeeze with month end rebalancing.. nice to be out of Canadian stocks now... credit isn't buying in the same way... have a nice we guys

- January 29, 2016 at 9:52 PM

- AL said...

- Congrats MM for the JPY call few days ago .... Certainly the trade of the week.

EURCHF and Bunds going bid simultaneously like there is no tomorrow in the last few days is clearly a hint that SNB has been doing the heavy lifting for the ECB on this front .... Especially today, with EZ flash CPI printing higher than expected.

Now, the stabilization that MM, LB and others invoked is happening and the missing piece of the puzzle is clearly the banking sector in EZ. Italian names have been hammered indiscriminately, but few of those are probably worth a look: remember that the Italian market has been the darling until only few weeks ago, before going through a torrid January. The newsflow has been bad, no doubt, but also positioning from HFs was kind of heavy and this has been probably washed out now.

Finally, I cannot push away the feeling that EM equities, in aggregate, are looking bid: here positioning is very light in terms of allocation in global portfolios and I see an opportunity of outperformance for the next 3/4 weeks. I increased the exposure here.

One last note: Norges Bank will buy 900 million NOK a day in February, almost double the amount of January. Such amount is not huge for the FX market, but if combined with a bid oil and a less risk averse environment, could make the NOK worth a punt. - January 29, 2016 at 10:09 PM

- TheBondStrategist said...

- @al: FtseMib had good result in 2015 but is under performing since the summer and banks are going down since the same period, isn'T a January story. FTSE today rebound is less than yesterday loss. No short seller haS been washed out.however bank credit haS recovered a lot, probably there's some arbitrage to play now.

I have the same feeling for em equities - January 29, 2016 at 10:34 PM

- Anonymous said...

- The Italian, Portuguese, Spanish and Irish bank balance sheets are muck. Hide the sausage is all they are playing.

For example, the Irish keep on extending interest only mortgages with no capital repayments. Extend and pretend, reduces default numbers. Then there's the almost total lack of repossessions. Government has resorted to restricting supply to bump up prices so banks can up their asset valuations. - January 29, 2016 at 11:01 PM

- Anonymous said...

- @TBS 10.44/12.08: Agree that NIRP doesn't belong on a straight line extrapolation from positive to zero rates, and may well be a bank killer if real reflection (ie. absent contrary QE) of true deflation. With shrinking balance sheets and lending. In long run may also crush asset prices with less money, credit and economic contraction. Assumptions that project past financial asset value-store trends into the future could also be killed.

But could be argued it's a reaction (not a cause) to what happens when too many people take more out than they put in, for too long. People probably including me to be fair.

northshore - January 29, 2016 at 11:09 PM

- Amplitudeisofftobettingshop said...

- Me think that the invisible hand of monetary golden eggs is in its last phase in this bull run in the US. Your right..we are witnessing Somalia pirate politics within the cabal of CBanks. " if you won't share your inflation with us...we'll share our deflation with you". It's been the warfare blueprint along.

Maybe Trump can implement fiscal managed growth and drag the Cbank cabal off the mat..b/c their f##cked. Their won't be another China growth story in our lifetime. - January 30, 2016 at 1:00 AM

- Anonymous said...

- Kuroda at Davos: "There are many financial assets in Japan, including government debt/bonds. The country's bond market is the biggest, most resilient, and deepest market."

He said the BOJ currently holds only one third of that market, so two thirds is still out there.

“If necessary to achieve the 2 percent inflation target, particularly if the underlying inflation trend is seriously affected, then we can expand or further strengthen QQE in many(!) ways. There are many(!) ways to further strengthen and expand QQE even more creatively.”

At the central bank, he has shown a tendency to surprise investors and BOJ watchers -- in the scale of his original asset-purchase program in April 2013, and in an unexpected expansion of the initiative in October 2014. Surprise is a very important element of the BOJ’s policy under Kuroda ...

From a recent Bloomberg interview - January 30, 2016 at 1:21 AM

- abee crombie said...

- For anyone looking for reasons to optimistic on asset prices, read/listen to black stones q4 call. Yes say what you may about PE and I'm sure schwartzman is talking his own book, just like everyone else, but it gives you some idea from someone who pays attention to the details on valuation and who also is one of the smartest guys in the room.

More earning on Monday, maybe Google / alphabet beats big as well and helps the market out of the funk? Let's see. Some of the companies who disappointed earlier seem to be catching a small bid especially those that are cheap and whose issues are well known, when those stocks turn it's usually a good sign sentiment has turned. But I wouldn't extrapolate one day to a trend just yet. But hey at least oil is holding above $30. - January 30, 2016 at 2:10 AM

- Eddie said...

- This might be a good way to think about CBs and their presumed or real abilities:

Wikipedia: Game of Common Knowledge. - January 30, 2016 at 10:14 AM

- Eddie said...

- Marco Man,

I hear you. Is there an easy way to calculated some normalized valuation measure (e.g. CAPE) for the MSCI in 1987 and compare it to its historical average? My argument is that if you buy a 9% bond way above par it yields only 6.5%... if the MSCI was sufficiently highly valued back then returns should be accordingly lower.

Again, thanks for your efforts. - January 30, 2016 at 10:25 AM

- Booger said...

- I think it is well known that returns have been juiced by central bank QE's.

But it is not clear that it will end soon. But when it does, it could be a real reset. So I agree that having a larger cash allocation makes sense from current values, but one would have to be extremely patient and be prepared for things to go up further if there is suddenly more QE.

I wonder if the signal for this will be political. For instance, in Japan, Abe would have to go and the population would have to vote for something radical like replacing QE & NIRP with legislated 5% wage inflation every year. But this would not be popular with business or asset owners, so it is hard seeing that getting political backing.

Then again QE does appear to be going nowhere and may well be deflationary. The idea of putting one's money in a bank to subsidize the bank to borrow from the BOJ, does not appear that attractive. And of course even the BOJ are running out of assets to buy. They say they are not limited to buying moar when they already own 1/3 JGB's (currently), but what is the limit, 1/2, 2/3, 3/4, 9/10th's, 99/100ths ? One would presume there is a limit at some stage and the Japanese may well be there in the next 3 years. It will be interesting to see what happens and it will set the tone for the rest of the QE world.

It is hard to say where USD.JPY will go. Either you believe the BOJ will do the logical thing, acknowledge their previous efforts have failed and back off. The current account & PPP would indicate yen should appreciate.

Or you believe the BOJ will continue to do the human thing, which is easier in some respects, but ultimately not so, and that is to say what we are doing works but we need more of it to work. That is what they have done to date, which is continue to do moar and devalue the yen despite the potential destabilizing systemic effects of further QE on JGB's. It's a pretty hard call I think, whether the BOJ will fire the last few bullets in the bear cave, with a good chance of blowing their own heads off in the process. They may well do that and drive the Yen into the ground or they and the Abe government may get booted out before that.

In either case, I think it is interesting to watch but there are easier assets to have conviction in than USD.JPY currently. - January 30, 2016 at 11:51 AM

- Booger said...

- What is truly shocking is Japanese YoY exports down 8% last month and industrial production has been dismal this year as well, despite the yen depreciating ! That is just terrible. As far as CB credibility goes, in financial markets well you follow the CB until they have to cave. I wonder whether the BOJ is losing credibility with the general population there.

- January 30, 2016 at 12:06 PM

- Booger said...

- http://cdn.meme.am/instances/400x/66397287.jpg

- January 30, 2016 at 12:25 PM

- Anonymous said...

- In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value. If there were, the government would have to make its holding illegal, as was done in the case of gold. If everyone decided, for example, to convert all his bank deposits to silver or copper or any other good, and thereafter declined to accept checks as payment for goods, bank deposits would lose their

purchasing power and government-created bank credit would be worthless as a claim on goods. The financial policy of the welfare state requires that there be no way for the owners of

wealth to protect themselves. […] This is the shabby secret of the welfare statists’ tirades against gold. Deficit spending is simply a scheme for the confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights.

If one grasps this, one has no difficulty in understanding the statists’ antagonism toward the gold standard.

– Alan Greenspan, former Chairman of the Federal Reserve - January 30, 2016 at 1:13 PM

- Bruce in Tennessee said...

- Well, interesting week, and to me all of the interest was from the BOJ. I look at devaluation as really tariffs disguised so they can go out at Halloween with the other children and not be called what they are. But they carry their little bucket to reap treats like everyone else.

Devaluation means our goods are more costly to the citizens of the devalued country...Hmmm...that might look like a tariff in disguise. We will sell less there...check. By inference their competitive good would do better here...check. And what does NIRP bring? Devaluation, one would expect. Tariffs mean you are a bad country, but devaluation? Not so much...

Is NIRP just the logical next step to ZIRP? To me this is unclear, but I'm trying to learn. I suppose here in the US many on the Fed will realize that the trend to ultra-low interest rates around the globe is not ending, as economies aren't doing particularly well under what has been tried so far. The question is, How will they think this through, and how will they respond?

It seems we can never kick the can far enough... - January 30, 2016 at 1:45 PM

- hipper said...

- NIRP is a by-product of lack of aggregate demand growth. Lack of growth doesn't mean people aren't still buying stuff, there's tons of stuff consumed, but rather just means people don't need to buy more stuff than they currently are. Devaluations across the globe are by itself manifestations of this and are targeted because there is no other growth to be had than steal it from neighbors. Just look at the anemic global trade growth.

So the other way they think that growth can be increased is by increasing (working age) population (this idea is certainly behind EU/US mass immigration process) which is probably true, however, it doesn't by itself mean that the new population could support itself. What I think is going to happen that the growth for increasing population must come through increasing government deficits. And while GDP increases, GDP per capita will go down in DM (kind of diluted), so it's basically a zero sum game. I don't think they'll find the Holy Grail from mass immigration but there will be tons of other problems. One thing which seems to have been totally disregarded is increasing productivity. If productivity is higher, then marginal demand increase won't increase employment as much as it did in the past. Or said another way, the same amount of population can be served by a smaller amount of human work than in the past. Since household income is important, this should be a bad thing.

So nothing points that the system in DM can withstand states deleveraging. Especially in the EZ most states are the absolute backbone of the economy and even keeping the economy from falling requires a certain amount of increasing leverage every year. That's why they are creating all these bureaucratic and useless government/muni jobs, it's part of having to invent ways to distribute the increasing debt as income to the population.

As the outstanding debt gets larger and there still is no inflation and thus no increase in tax revenues, interest rates need to go lower in order to keep the "hide the Sausage game" going and not blow up from larger outstanding debt levels. They are trapped in a vicious circle of increasing the tax proportion of the total economy further straining growth, insufficient growth, lack of (benevolent) inflation and continously rising debt. Hence the only thing that can give way is the interest rate. In a historical perspective (just a gut feeling) is that with the absence of growth, the end game, whatever it might be, is approaching at warp speeds compared to the past of higher growth and more new innovations driving demand. - January 30, 2016 at 3:49 PM

- abee crombie said...

- NIRP to me is a message to FX traders and wealth, don't sit on this currency or I will hurt you. It's a tactic by cb to get the big guys to do something. fx punters don't care, they will move with or against cb when they feel like it. But corporate and real money feel the pain and have to go out on the risk curve or into another currency. To me it just says buy equities please bc if you don't I will tax you.

I agree this isn't optimal policy making, it's beggar thy neighbor tactics but I don't see much way out of it. Remember yen trade weighted index was back below qE levels. Japan is in this qE game all in, I'm not sure they can do much else. If they turn back on it it would be devastating for equities there. But equities in Japan are only getting killed bc global ip is in the dumps. Get the economy to stabilize and just stop going down and I think you will see a nice rebound there as cyclicals in Japan have gotten beat up like in most countries.

Ism on Monday will be the first test. Chicago was a big surprise. A number above 50 could light a fire under many shorts. - January 30, 2016 at 8:26 PM

- Booger said...

- So we have Japanese QE (constrained, maybe reaching end point of further expansion), Euro QE (still March expansion to go) Vs Oil SWF and BRIC selling.

ZIRP is not quite the asset juicer that QE is so one would suspect this rally fades. Perhaps there is another rally in March with euro QE expansion, but it's hard to see much after that keeping things afloat for the S&P, which might be a good short again around 2020. - January 30, 2016 at 9:26 PM

- Basho said...

Perhaps the BOJ, sooner or later, will turn their attention to overseas assets. No shortage of targets there.

As hipper noted, all this activity (QE, ZIRP, NIRP and so on) has as its principal goal generating aggregate demand growth. And yet, isn't this entire suite of policies a kind of category error? Sustainable demand is weak principally because it's been artificially goosed for decades by credit growth far in excess of GDP growth. Having thereby brought forward mountains of future demand into the present (now the past), the bill, it seems, has finally arrived. Ploughing deeper into this structural cul de sac by trying to force yet more credit growth down the world's throat doesn't strike me as a high probability bet.

Still, realistically, what are the powers that be to do? 'Fess up and let things fall where they may? Given a powerful deflationary undertow will be with us until debt/GDP ratios are by one means or another restored to sustainable levels, I sometimes wonder if, given current political realities and economic paradigms, there isn't only one way "out". Namely, hammer currencies hard enough and long enough to produce a mild revulsion and thereby get velocity up and running. A sort of deliberately induced "crackup boom".

That should "do it" but whether the beast can be controlled once it's out of its cage is another matter. In any event, if any country is likely to give it a whirl, it's probably Japan.- January 30, 2016 at 11:30 PM

- abee crombie said...

- Agreed basho. Govts will end up spending and finally get inflation, imo ...there is nothing stopping them just the misguided belief that government debt is like personal or corporate debt. ...James monitor wrote a recent piece on it.

But politicans and the general public doesn't like it. So maybe we need them to get really scared before they do it. - January 31, 2016 at 1:56 AM

- Basho said...

Abee, I should perhaps have made it clearer this isn't a policy I favour. It's just the one that may well be followed after all else they're willing to try fails.

The Montier argument is true to a point. Indeed, the best of the MMT crowd seem to have an exceptionally good grasp of monetary mechanics. Still, the central challenge of enabling the sustainable coordination of economic activity is in my view harmed, not helped, by all these monetary gyrations.- January 31, 2016 at 4:29 AM

- Anonymous said...

- Of course, if a government decides to just give every citizen 100,000 units of its currency. They create an inflation right away. The question is, are they crazy enough to do this?

- January 31, 2016 at 4:32 AM

- Anonymous said...

- Basic income is being bandied about... That qualifies as helicopter?

- January 31, 2016 at 5:37 AM

- Booger said...

- Anon 4:32, during the GFC, some countries had a bonus of a few k per citizen to get things going. No reason you couldn't give citizens say 20k per year for 5 years which they must spend on consumption or forfeit. Or alternatively legislate for say minimum 5% wage increases per year. But really this is all too desperate. One wonders whether just having a recession, cleanout and writing down of debt would just be lot quicker.

No the problem is not inflation which can be generated, but mild price inflation with ongoing asset price inflation that CB's want that is hard to cook in this environment - January 31, 2016 at 11:11 AM

- fe2plus said...

- Well, either oecd countries raise their fertility rates to 2,1 to stabilize the demographics or they start systemically monetizing debt to facilitate respectable end of life care to societies going extinct.

Mass immigration isn't the solution many thought it would be, in fact long term it makes things worse (immigrant TFRs converge with natives')

QE isn't doing what it's supposed to and IMO is a much more perverse remedy than outright helicopter drops.

Now we wait for the Japanese to figure it out so the rest of us can follow. - January 31, 2016 at 12:55 PM

- Anonymous said...

- At a conference hosted by the BOJ last year, Kuroda cited Peter Pan for inspiration.

“I trust that many of you are familiar with the story of Peter Pan, in which it says, ‘the moment you doubt whether you can fly, you cease forever to be able to do it," he said at the time.

For Kuroda, with subdued wage growth and falling oil prices, reaching his key inflation goal looks as far away as ever.

http://www.bloomberg.com/news/articles/2016-01-31/boj-market-magician-kuroda-pulls-yet-another-rabbit-from-his-hat - January 31, 2016 at 4:51 PM

- TheBondStrategist said...

- Positive comment from Davies on FT...

http://blogs.ft.com/gavyndavies/2016/01/31/bank-of-japan-tries-another-flavour-of-qe/

i'm skeptical...according to me he's missing the impact of negative rates on govies owned by banks but maybe i'm wrong.

What these economists are missing is not the fact that CB are out of ammonitions, but that these ammunitions have a limited (if any) impact, and maybe dangerous policitally and for the stability of financial markets.. let's the time be the judge - January 31, 2016 at 5:28 PM

- Anonymous said...

- All this sh*t that govt debt is not like personal debt, is just that - sh*t.

Look if printing money was the cure-all Zimbabwe would be the richest country in the world, followed by Argentina etc. F*ckwit economists and people in Finance with no brain need to stop this nonsense asap. If anyone thinks QE, ZIRP and any form of CB induced inflation is a good idea, they are utter f*ckwits of the highest order.

Have I made my point clearly? - January 31, 2016 at 8:30 PM

- Anonymous said...

- You will ask, what are countries to do in the face of BOJ 'beggar-thy-neighbor' policies?

The answer is simple. If I were China I would impose catastrophic tariffs on Japanese goods and then launch military operations against them. I am deadly serious. In fact these beggar-thy-neighbor' policies were the precursor to previous conflicts. If Japan were destroyed (financially and/or militarily by China they only have themselves to blame. - January 31, 2016 at 8:38 PM

- amplitudeinthehouse said...

- F##k off! and you think I'm going to walk down the aisle with that dumbo trade. Leave me out one the street again. Take all your computer models and jam'em , this market won't play the keynesian look at me popularity contest. It's a dunce with a rich daddy(central banker) market..period.

- January 31, 2016 at 10:13 PM

- Anonymous said...

- Re: qe

Are those negative rates policies /qe aimed at maintaining asset valuations ticking up or at creating organic sources of healthy growth ( which logically should be done via fiscal and structural reform ) ?

It seems obvious that high to very high asset prices ( real estate in major cities an exemple but there are plenty others ) are creating a need for ever growing cash flow to service those valuations.

What we need is a valuation and debt reset and start from fresh.

After all, GDP growth is measured as a difference btw two prices .

For exemple, Policymakers and regulators should be focusing at creating the tools to allow some default without fear of the whole system collapsing .

Basically, we should not forget the longer term trend of the past 30 years and the next 30: DM economies are converging towards EM economies and vice versa. There are bumps on the road but certainly many DM workers are seeing their earning power and wealth converge towards the one of workers from EM who actually manufacture what we all buy everyday in Europe/US . If you buy 90 % of your goods from a Chinese worker , how come you can still earn more than him for ever. Only of fraction of Europe /us jobs can commend a premium for so long . ( yes EM doesn't look so good at the moment but the big trend is still ongoing and it will continue to not feel nice for most DM workers so you may as well help them be more competitive by lowering the cost of living/ doing business like how much you need to pay staff just so they can pay the rent, commute, healthcare etc...)

No immediate trade to implement out of that though sorry!

Travis - January 31, 2016 at 10:19 PM

- Amplitudeisofftobettingshop said...

- What blog are we running here..are we running match.com for speculators versus QE initiators. It's over..the quantitative 20% drives north, the clandestine high frequency trades operating under the wall street exchange have moved into university dorms, the markets capacity for flash crashes have been reduced due to circuit breakers. The fun is over, no one cares about computer model driven markets. Its time for solid fundamental analysis. Shove your computer model driven market through into the next kalpa. I'm off to study for the next 20% move..

- January 31, 2016 at 10:35 PM

- Anonymous said...

- Amps ... do let us know how you finally decided to position yourself for that next 20% move. Gold? Oil? TLT? IWM? NLY?

- February 1, 2016 at 1:09 AM

- abee crombie said...

- I agree that the QE drug is having less of an effect but one should not forget that we are pretty much in an economic slowdown right now. If we bounce out of it (ie some positive surprises) the sentiment is pretty bearish and could cause a nice pop. As well, the S&P was down 10% after a 7 year bull market. WOW. Everyone predicting the next crash might want to put things in perspective first. Even if we went down 20%, big deal. Its happened before and the economy and markets survived.

Back to the markets, what are ppl's watch levels on Spoos or other markets.

Russell has a nice H&S with a neckline coming up soon around soon, maxed out at 1100 pr 6% higher. If ones thesis that the markets are cheap enough to attract bargain hunters is correct than Russell should outperform and nullify that level and lead Spoo's to the upside. We should know this week. I'm waiting. My big test will be Spoo's at 150/200 day moving average but 1980 seems like the first big test if we can make it there. - February 1, 2016 at 5:18 AM

- Nico G said...

- the loonie the loonie is baaack

- February 1, 2016 at 5:57 AM

- Nico G said...

- abee

things ain't looking that rosy in Europe at all. From a constructive bounce price action the previous two weeks we have seen a monumental miss in Stoxx and Dax. When Europe starts underperforming a global bounce amid a correction landscape this is the time to dust off the bear suit. I am going to be shorting clips of stoxx from today onward

i have no idea if we'll see 20% down on spoos this quarter but market does need to go test the 1800s again and see if they can floor it for some time

Monday, February 1, 2016

qe It seems obvious that high to very high asset prices ( real estate in major cities an exemple but there are plenty others ) are creating a need for ever growing cash flow to service those valuations.

116 comments:

{kind=link}

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment